I spent a few years working on drug cases when I was a prosecutor, so I was generally aware that North Carolina has a set of laws that impose taxes on “unauthorized substances.” See G.S. 105-113.105 – 113. Just like cigarettes, cars, or blue jeans, these unauthorized substances are commodities that people buy and sell, so they are subject to taxation by the state.

I was also aware that, not surprisingly, virtually no one pays these taxes or obtains the appropriate “tax stamps” to put on their drugs and moonshine. Instead, the laws are used primarily as a mechanism to pursue civil forfeiture of a defendant’s assets after he or she is convicted of a drug offense.

But recently, I began to wonder – are these laws purely theoretical? Is it even possible for drug dealers to comply? Does the Department of Revenue keep big rolls of stamps behind the counter, like a post office? What would happen if someone walked into a Revenue office one day and said “hello, will you sell me some tax stamps for illegal substances, please?”

I wanted to find out, so that’s exactly what I did.

Overview of Drug Tax Laws

If you’re curious about these laws, the Department of Revenue has a helpful FAQ available here.

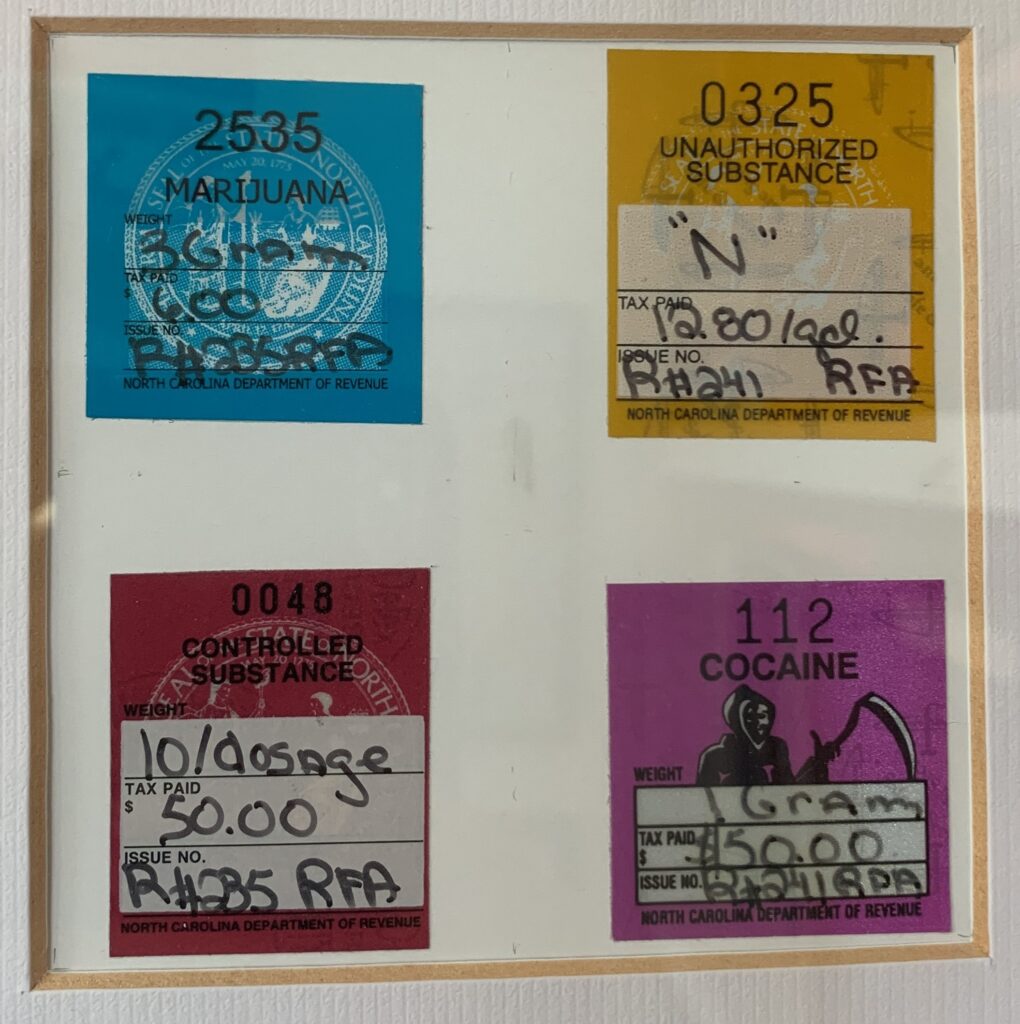

Briefly, these laws only apply to a “dealer,” which is defined as a person who possesses more than X amount of certain drugs (e.g., 42.5 grams of marijuana, 7 grams of a drug sold by weight such as cocaine, 10 doses or more of a drug that is not sold by weight such as LSD, or any amount of an illicit spirituous liquor such as moonshine). See G.S. 105-113.106. If a person is in possession of the minimum amount, then he or she is obligated to pay taxes on that substance within 48 hours of when it first came into his or her possession (excluding weekends and holidays), pursuant to the statutory rate schedule (e.g., $50 per gram of cocaine, or $12.80 per gallon of liquor not sold by the drink). See G.S. 105-113.107; 113.109. The Department has this handy reference chart of tax rates available online.

Once the tax has been paid, and a tax stamp issued by the Department has been “permanently affixed” to the substance, no further tax is due – even if the substance later changes hands. See G.S. 105-113.108; 113.109. As noted above, if a dealer fails to pay the tax when it’s due, he or she is subject to an “assessment” (including penalties and interest, which can be as high as 40%) to recover the unpaid tax. See G.S. 105-113.111 (“The Secretary shall use all means available to collect the tax, penalty and interest from any property in which the dealer has a legal, equitable, or beneficial interest”).

Of course, paying the tax does not change the fact that the substances themselves are still illegal, and the person in possession of that substance remains subject to criminal prosecution. See G.S. 105-113.105. Therefore, to facilitate compliance with the tax laws, dealers are not required to give their name, address, or any other personal identifying information in order to obtain stamps. See G.S. 105-113.108. Furthermore, any information obtained by the Department in the course of administering these laws is considered confidential tax information, and it may not be used in a criminal prosecution; in fact, any agent or employee who violates this prohibition is guilty of a Class 1 misdemeanor. See G.S. 105-113.112; State v. Stimson, 246 N.C. App. 708 (2016).

What About Double Jeopardy and the 5th Amendment?

The tax rates set by an early version of the law were so high ($200,000 per kilogram of cocaine) that the Fourth Circuit held it constituted a criminal punishment, which would implicate double jeopardy. See Lynn v. West, 134 F.3d 582 (4th Cir. 1998). But the rates were revised down, and subsequent North Carolina cases have pretty consistently held that this is a civil remedy, not a criminal penalty, and it passes constitutional muster on double jeopardy and self-incrimination grounds. See, e.g., North Carolina School Board Ass’n v. Moore, 359 N.C. 474 (2005); State v. Woods, 136 N.C. App. 386 (2000); State v. Adams, 132 N.C. App. 819 (1999); Milligan v. State, 135 N.C. App. 781 (1999).

The Court of Appeals summed it up this way: “In our view, the North Carolina statute is a legitimate and remedial effort to recover revenue from those persons who would otherwise escape taxation when engaging in the highly profitable, but illicit and sometimes deadly activity of possessing, delivering, selling or manufacturing large quantities of controlled drugs.” State v. Ballenger, 123 N.C. App. 179 (1996).

Do These Laws Actually Work?

Well, that depends on what we mean by “work.” Do they generate money for the state? Absolutely – as shown in this summary report covering 2002-2016, the total revenue generated by these taxes typically ranges from a low of around $6 million to a high of around $11 million per year. By statute, 75% of this revenue goes back to the law enforcement agency that conducted the investigation which led to the assessment, and the remaining 25% goes into the state’s general fund. See G.S. 105-113.113; see also G.S. 105-113.108(b) (law enforcement agencies must report drug seizures and related arrests to the Department involving unauthorized substances “upon which a stamp has not been affixed as required by this Article”).

However, if by “work” we mean “are drug dealers purchasing tax stamps and permanently affixing them to their unauthorized substances in a timely fashion,” the answer, of course, is no. In this WRAL interview, the Director of Tax Enforcement for the Department of Revenue, Cale Johnson, explained that out of the 5,000 to 6,000 cases they handle every year, they have only received a grand total of 109 orders for stamps since the program began back in the 1990s, and they “believe a majority of those orders were from stamp collectors.” That interview was given in 2010, so the total may be a little higher today, but clearly the number of people buying stamps is only a tiny fraction of the total cases. The rest of them are “assessments” on dealers who failed to buy their stamps.

What Happened When I Tried to Buy Stamps

Just to be clear, I am not currently in possession of any unauthorized substances, nor do I plan to be. But I wanted to see how well the process would work for someone who was genuinely trying to comply with the law. So on a Thursday afternoon, around 1:30 p.m., I stopped by my local Revenue office to find out. It was located in a nondescript shopping center behind a Korean BBQ restaurant.

Although the statutes say that a person can obtain tax stamps anonymously, I quickly ran into my first obstacle on that issue. As soon as I walked in the door of the Revenue office, I saw a table with a sign instructing me to fill out a form with my name, social security number, address, phone number, and the reason for my visit. I was instructed to give that form to the clerk at the window, and then wait to be called up.

I filled out the form, and in a minute or two a very nice clerk called me up to the window and said “how can I help you?” I said “Good afternoon, do you sell unauthorized substance tax stamps here?” Her eyes got very wide, she hesitated a little, and said “uh… no. Maybe downtown at the main office, but I don’t think so. Here, call this number and ask them.” She wrote down the phone number for the Unauthorized Substance Tax Section on a post-it note and handed it to me. I don’t know what happened to my sign-in form after I left.

I stepped outside and called the number she gave me. A woman answered, and I said I had a question about buying unauthorized substance tax stamps. She asked me what my pending case number was? I explained that no, there is no pending forfeiture case – I’m just interested in buying some actual stamps? (Pause…) She said I would have to talk to a director about that, but if I will leave my name and home phone number, somebody will call me back.

About 30 minutes later, I got a call back from a Charlotte number, and a woman who introduced herself as “Look, I’m just a secretary here” said that I should go on their website and search for Form BD-1, print it out, fill it in, mail it to their office, and I could get the tax stamps sent back to me. I asked if there was any way to get them in person, today? She said not that I’m aware of.

I searched online and realized there are actually two forms. The first form, BD-1, is for illegal drugs like marijuana and cocaine. The second form, BD-1L, is for illicit spirituous liquors. Both forms ask the applicant to fill out his or her name, phone number, and mailing address. (After all, how else will they send the stamps back to you?) Then the form cites to the statute that says a person is not required to give his or her name, address, or any other identifying information in order to buy stamps.

G.S. 105-113.109 states that the tax is due within 48 hours of whenever the drugs come into a dealer’s possession, so it is a little difficult to see how ordering stamps through the mail (anonymously or otherwise) would enable a dealer to fully comply. Thinking that I may have missed something, I called back again the next day just to follow-up and make sure there were no other options for acquiring the stamps in person, or on a shorter time-frame? This time I was told that it used to be possible to purchase stamps directly at the main office in Raleigh, but they don’t do that anymore. As far as she knew, the BD-1 and BD-1L forms are the only option now.

End of the Road

I’d really like to have a couple stamps to keep in my office as a curiosity, but I’m hesitant to take the final step of filling out the form and mailing it in. I am not aware of any law that would prohibit me from voluntarily paying a tax I don’t owe just to get the stamps, but my instinct tells me that it’s probably not a smart career move to end up on that list.

I doubt there is much sympathy out there for drug dealers who end up facing a hefty tax assessment with added penalties and interest, but I do have to wonder whether some of the cases interpreting these laws might be based, at least in part, on an underlying assumption that the dealer could have easily and anonymously complied with the law and simply failed to do so. My personal experience suggests that compliance with these laws may not be quite as easy as it sounds.

Thanks to SOG Defender Educator Phil Dixon for his assistance with this post.

UPDATE: The Department of Revenue FAQ page linked above now indicates that stamps may be purchased “in person at a service center, between the hours of 8am and 5pm, Monday through Friday.”